Under the ledger (COLB)

The Bank the Market Is Reading Wrong

Forward

The Bank the Market Is Reading Wrong

This report is an updated version of our initial COLB analysis. Following a conversation with The M&A Hunter — a Substack newsletter specialising in acquisition targets across banking and biotech — we identified two important refinements: the Q4 NIM figure requires context that our initial report did not provide, and the M&A angle on COLB deserves its own section. Both are incorporated here.

Columbia Banking System is the bank where GAAP earnings look messy — weighed down by acquisition costs, CDI amortisation, and one-time charges — while the underlying operating performance is quietly excellent. The market reads the headline number and moves on. The CPA opens the footnotes.

At $26, trading at 7.5x forward operating earnings and yielding 5.7%, COLB is the kind of mispricing that does not last.

1. Executive Summary

COLB trades near the middle of its 52-week range at approximately $26 — well below its August 2025 high of $32.70. The decline reflects regional bank sector weakness and investor caution around Pacific Premier integration. The actual financial results tell a different story.

What the market believes:

Pacific Premier integration costs are elevated. Q4 NIM of 4.06% was artificially inflated by one-time items and will fall in Q1 2026. Loan growth is muted. The CFO departed at year-end. Regional banks face headwinds from potential credit deterioration. The dividend was flat for five years and cannot be trusted.

What we believe:

Yes — Q4 NIM included an 11bps one-time benefit and Q1 2026 will print 3.90-3.95%. That is not deterioration. Core NIM of 3.95% is still best in the peer group and expanding. Management guided NIM above 4.0% again in Q2-Q3 2026 as synergies complete. Operating EPS of $3.25 in FY2025 is growing to $3.48 in FY2026. Tangible book value grew 11% year over year to $19.11. The dividend restart after five flat years signals confidence. The buyback is real — $150-200M per quarter.

Three catalysts for re-rating:

• Q1 2026 earnings on April 23 — NIM stabilising at 3.90-3.95% confirms the core story; any upside surprise re-rates sharply

• Full synergy realisation by H2 2026 — $127M pretax in cost saves fully captured, operating leverage accelerates

• M&A premium optionality — $7.8B market cap with top-10 Southern California deposits is exactly where large bank acquirers look

The one risk that makes this thesis wrong:

A US recession driving credit losses materially above current levels — particularly in FinPac small-ticket leasing (elevated Q4 net charge-offs) and the 8% office loan exposure. A hard landing raises provisions and compresses EPS.

2. Investment Thesis

2.1 The GAAP vs. Operating EPS Gap — The CPA’s Edge

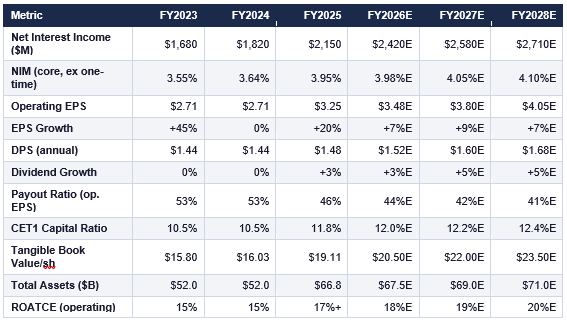

This is the most important analytical point in this report. GAAP EPS for FY2025 was approximately $2.30. Operating EPS — stripping out merger costs, CDI amortisation, and a legal settlement — was $3.25. The gap is driven entirely by non-recurring acquisition items.

At $26 per share, COLB trades at 11.3x GAAP earnings — which looks fair. At 7.5x operating earnings — which looks cheap. By 2026 as acquisition costs roll off, the two numbers converge. Investors who wait for that clarity will pay a higher price.

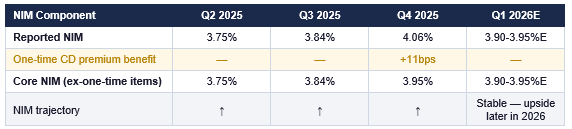

2.2 The NIM Story — What Q4 Actually Tells Us

This section addresses the most important correction from our initial report. Q4 2025 NIM was reported as 4.06% — a 22 basis point sequential improvement. However management disclosed that this figure included two one-time benefits that will not repeat in 2026:

• $12M in premium amortisation tied to acquired Pacific Premier time deposits — contributed approximately 8bps

• $5M from an accelerated loan repayment — contributed approximately 3bps

• Total one-time benefit: approximately 11bps

Core NIM — excluding these items — was approximately 3.95%. Management guided Q1 2026 NIM at 3.90-3.95%, reflecting the absence of these one-time benefits plus typical seasonal deposit weakness in Q1.

This is not a negative development. Core NIM of 3.95% is still the best in the peer group. And management explicitly guided NIM to exceed 4.0% again in Q2 or Q3 2026 as the remaining Pacific Premier cost synergies complete and deposit pricing improves. The trajectory is intact — just one quarter delayed.

NIM trajectory — quarterly breakdown:

2.3 The Pacific Premier Acquisition — Delivering

Columbia acquired Pacific Premier on August 31, 2025. The deal created a $66.8B asset bank with 350+ locations across eight western states. Systems integration completed Q1 2026 — the highest-risk phase is behind the company.

Key delivery metrics:

• New loan origination volume: up 22% full-year 2025 vs 2024 — commercial banking pipeline is strong

• 1,200+ cross-sell referrals generated since closing — HOA banking and custodial trust adding fee income

• Operating PPNR up 27% sequentially in Q4 2025 — full quarter of Pacific Premier at run-rate

• $127M in pretax cost synergies targeted by June 2026 — tracking ahead of schedule

2.4 The M&A Premium — An Additional Return Scenario

This angle was flagged by The M&A Hunter (@maandhunter on Substack), a newsletter specialising in acquisition target identification across banking and biotech. The observation: COLB sits precisely in the acquisition sweet spot for a large bank seeking Western US exposure.

M&A ANGLE — flagged by The M&A Hunter (@maandhunter)

The M&A Hunter — a Substack newsletter tracking acquisition targets in banking and biotech — flagged COLB as sitting in the acquisition sweet spot: clean balance sheet, strong geography, and a market cap ($7.8B) that is large enough to be meaningful but small enough to be digestible for a top-20 US bank seeking Western exposure. COLB started as an M&A target itself before becoming a buyer of Pacific Premier. With a top-10 Southern California deposit position now in hand, the strategic logic for a larger acquirer is compelling. A typical regional bank acquisition premium of 30-50% above market would imply a takeout price of $34-39 per share — providing an additional return scenario beyond the organic dividend thesis.

3. Business Description

3.1 What Columbia Banking System Does

Columbia Banking System is the holding company for Columbia Bank — the largest bank headquartered in the Pacific Northwest. Following Pacific Premier, Columbia operates with $66.8B in total assets, $47.8B in loans, and $54.2B in deposits across 350+ locations in eight western states.

3.2 Revenue Composition

Net interest income is the dominant revenue driver — approximately 87% of total revenue. Non-interest income of $90M in Q4 2025 is growing as Pacific Premier’s speciality businesses contribute: commercial card and treasury management fees rose year over year, and trust and financial services revenues expanded notably. Card, financial services and trust now comprise nearly 34% of non-interest income.

3.3 Credit Quality — The FinPac Watch

Overall credit quality remained stable throughout 2025 — COLB was, in management’s words, ‘untouched by external events that negatively impacted some peer banks.’ The allowance for credit losses was $485M or 1.02% of loans as of December 31, 2025.

However two specific areas warrant monitoring:

• FinPac small-ticket leasing — experienced higher loss content with sequentially higher Q4 net charge-offs. Management is targeting a normalised loss rate of 3.5-4% for FinPac. Any deterioration above this range signals stress in the small business segment

• Office loans — represent 8% of total loans. Office CRE remains under pressure nationally as remote work reduces occupancy. COLB’s office exposure is primarily in Western US markets which have held better than coastal gateway cities, but this warrants quarterly monitoring

4. Financial Summary

All figures in USD. E = Estimate. NIM figures show core NIM excluding one-time items. FY2025 tangible book value updated to $19.11 per share (Q4 2025 actual — up 11% YoY). Operating EPS excludes merger costs and CDI amortisation.

5. Valuation

5.1 Primary: P/E on Operating Earnings

Regional bank peers trade at 10-11x forward operating EPS. At 7.5x FY2026E operating EPS of $3.48, COLB carries a 27% discount to peers. This discount is partially justified by integration uncertainty — but not by 27%.

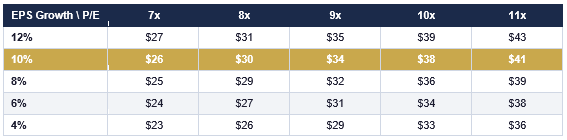

At a normalised 9.5x P/E on FY2026E operating EPS of $3.48:

→ Fair Value at 9.5x P/E: $33 per share

→ Price Target: $34 (reflects integration execution premium and M&A optionality)

5.2 Sensitivity Table — Fair Value per Share

Rows = FY2026E operating EPS growth. Columns = P/E multiple applied. Base case highlighted in gold (10% EPS growth, 9x P/E). Current price $26.

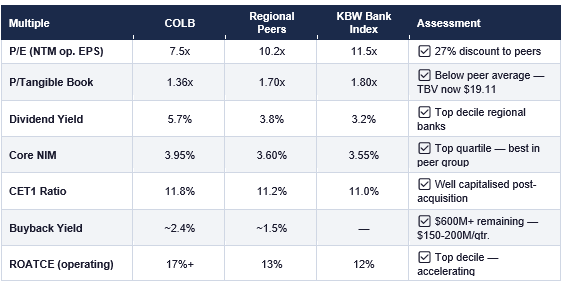

5.3 Relative Valuation

COLB trades at a meaningful discount across every metric. Note: P/TBV updated to reflect $19.11 tangible book value as of Q4 2025.

5.4 Tangible Book Value — Updated

Tangible book value per share grew to $19.11 as of December 31, 2025 — up 3% sequentially from Q3 and up 11% year over year. Our initial report used $17.86 which was the Q2 2025 figure. At current price of $26, COLB trades at 1.36x tangible book versus the peer average of 1.70-1.80x. Reversion to 1.65x TBV alone implies a price of $31.50.

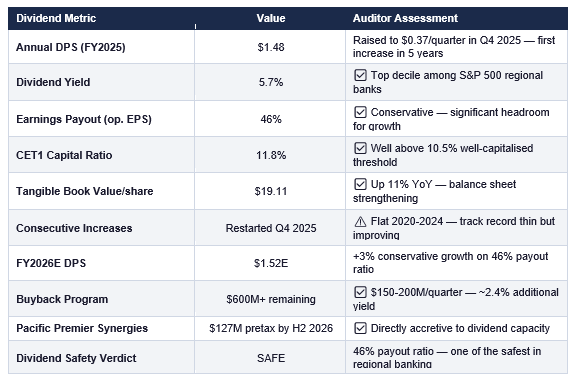

6. Dividend Analysis — The Audit

For regional banks the dividend audit requires an additional lens: can the capital structure sustain the dividend through a credit cycle? Columbia passes this test more convincingly than most peers with a 46% operating payout ratio.

6.1 Why the 5-Year Flat Dividend Is Not a Disqualifier

COLB held its dividend flat from 2020 through Q3 2025. The flat dividend reflected deliberate capital conservation through the Umpqua merger integration (2023), rising rate environment management, and Pacific Premier acquisition financing (2025). In each case management prioritised balance sheet strength over dividend growth. That is exactly what a CPA wants to see.

The Q4 2025 raise to $0.37 per quarter is the signal that the conservation phase is over. With a 46% payout ratio and growing operating EPS, dividend growth of 5-8% annually is entirely fundable without any payout ratio expansion.

6.2 Forward Dividend Projection

At 5% annual dividend growth from the current $1.48 annualised base at a $26 purchase price:

• 2027: $1.60 — yield on cost 6.2%

• 2029: $1.76 — yield on cost 6.8%

• 2031: $1.94 — yield on cost 7.5%

• 2036: $2.48 — yield on cost 9.5%

7. Risk Factors

7.1 Downside Risks

① Credit cycle deterioration — HIGH probability concern if recession, HIGH impact

COLB’s $47.8B loan book is exposed to Western US commercial real estate and C&I lending. A recession driving unemployment above 6% would increase non-performing loans and require elevated provisions. Two specific areas: FinPac small-ticket leasing (elevated Q4 charge-offs already) and office CRE (8% of loans).

② NIM compression from rate cuts — MEDIUM probability, LOW-MEDIUM impact

COLB guided Q1 2026 NIM at 3.90-3.95% — already below Q4’s 4.06% due to absence of one-time items. Further Fed rate cuts would compress NIM modestly. Each 25bps cut reduces NIM by approximately 3-5bps. Partially offset by lower deposit costs.

③ Integration execution — LOW probability post Q1 2026, MEDIUM impact

Systems integration completed Q1 2026. Primary remaining risk is cultural integration and talent retention from Pacific Premier. CFO departure at year-end is a modest concern — Ivan Seda brings strong credentials from MUFG and BECU.

④ NIM Q1 disappointment — MEDIUM probability, LOW impact

If Q1 2026 NIM prints below 3.90% due to seasonal deposit weakness or pricing pressure from competitors, sentiment turns negative even though the core thesis is unchanged. This is the most likely near-term noise event.

7.2 Upside Risks

• NIM above 4.0% ahead of schedule — if deposit repricing accelerates and wholesale funding reduces faster than guided

• Loan growth inflection — commercial banking pipeline in SoCal and Pacific Northwest stronger than guided; transactional runoff completes faster

• M&A premium — $7.8B market cap with top-10 SoCal deposits is an acquisition target; 30-50% takeout premium = $34-39/share

• Fed holds rates longer — NIM stability above 4.0% for longer re-rates the stock toward 10x+ P/E

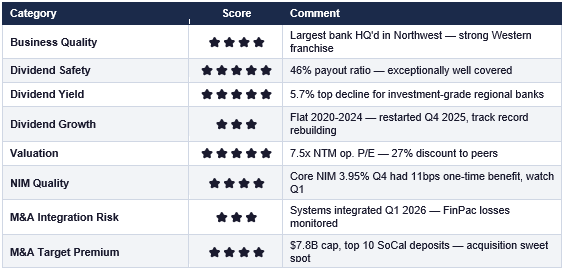

8. Summary Scorecard

Rated 1-5 stars across eight dimensions. M&A target premium added as a bank-specific metric following The M&A Hunter’s analysis.

9. The Auditor’s Verdict

VERDICT: BUY | $34 PRICE TARGET | +31% UPSIDE

Columbia Banking System is a classic CPA buy — where the accounting noise obscures a genuinely improving business. GAAP EPS of $2.30 hides operating EPS of $3.25. Reported Q4 NIM of 4.06% included an 11bps one-time benefit — but even the core NIM of 3.95% is best in the peer group and expanding. Tangible book value grew 11% year over year to $19.11. The dividend was raised for the first time in five years. $600M+ in buybacks authorised at $150-200M per quarter. At 7.5x forward operating earnings with a 5.7% yield, the market is pricing this like a broken bank. The balance sheet says the opposite. The one risk that makes this wrong: a US recession driving credit losses above current levels — particularly in FinPac small-ticket leasing and the 8% office loan exposure. Watch Q1 2026 credit quality metrics on April 23 carefully. Note on NIM: Q1 2026 NIM will likely print 3.90-3.95% — below Q4’s 4.06% due to the absence of one-time benefits. This is not deterioration. It is normalisation. The path to sustained 4%+ NIM resumes in Q2-Q3 2026.

DISCLAIMER: This report is produced by The Dividend Auditor under the ‘Under the Ledger’ series for informational and educational purposes only. It does not constitute financial advice or a recommendation to buy or sell any security. The author is a CPA, not a licensed investment adviser. Always conduct your own due diligence. The author holds a position in Peoples Bancorp (PEBO), a peer company. No position held in COLB at time of writing. The M&A Hunter reference is for informational purposes — full credit and link to maandhunter.substack.com.